Treasury nominee Timothy Geithner had several tax issues that are mentioned in this matter of fact Senate Report.

Among Tim Geithner's chief tax problems are:

Geithner prepared his own return in 2000, 2001, 2002, and 2005. Wednesday Geithner disclosed that he used TurboTax.1. Geithner's failure to pay self-employment taxes in the years 2001-2004 on his IMF income.

2. Geithner's taking a dependent care credit for the costs of overnight camp in 2001, 2004, and 2005.

I wondered how plausible it was that TurboTax wouldn't prompt Geithner adequately on these issues (there was also a suggestion that he may have been misled by improper advice from a tax preparer, despite the repeated information released from the IMF on his need to pay self-employment taxes).

To explore these issues, I installed both the 2004 and 2005 TurboTax on my new Dell Latitude E4200 (2.25 lb. notebook).

SELF EMPLOYMENT TAXES.

If Geithner's IMF income were entered from a 1099-MISC (which it wasn't), the self-employment tax would have been automatically added; he would have had to override it manually to avoid the SE tax.

But that is not how the IMF reported Geithner's income. They used a W-2, with "NONE" or blanks in all boxes except wages. In both the 2004 and 2005 TurboTax program, if you enter income only from a W-2, it does NOT add that income to schedule C and it does NOT compute a self-employment tax.

So, while technically TurboTax did not make a "mistake," TurboTax would have neither computed the SE tax automatically, nor would it have prompted Geithner appropriately that he needed to pay that SE tax. In other words, any knowledge of Geithner's SE liability would not have come from the usual TurboTax guided interview, but rather from the IMF.

OVERNIGHT SUMMER CAMP.

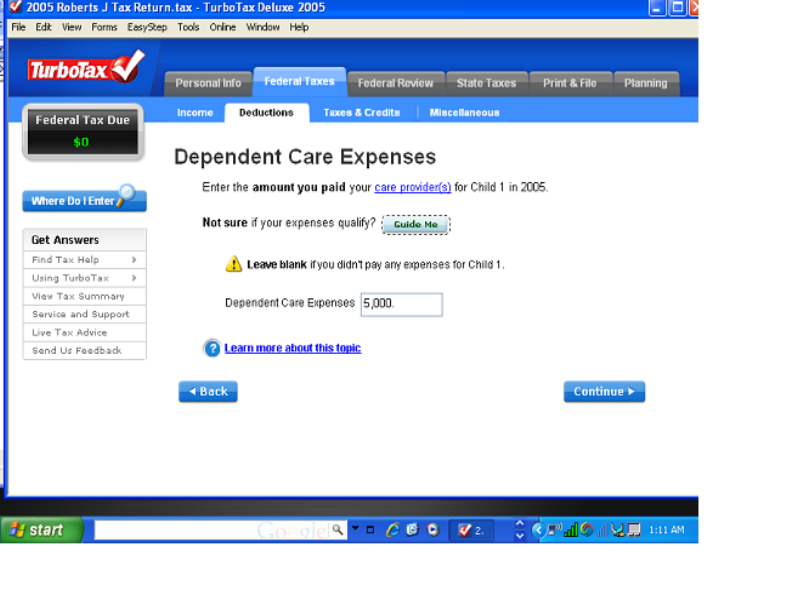

Geithner took a dependent care credit for the costs of overnight camp in 2001, 2004, and 2005. If one takes the normal interview process in TurboTax, it just prompts you for the amount. If you are "Not sure if your expenses qualify," you can click "Guide Me." The steps involved in that sub-interview do not ask about camp, but rather covers information about the child and the parents.

Screenshot from 2005 TurboTax

(click once to open, and then again to read)

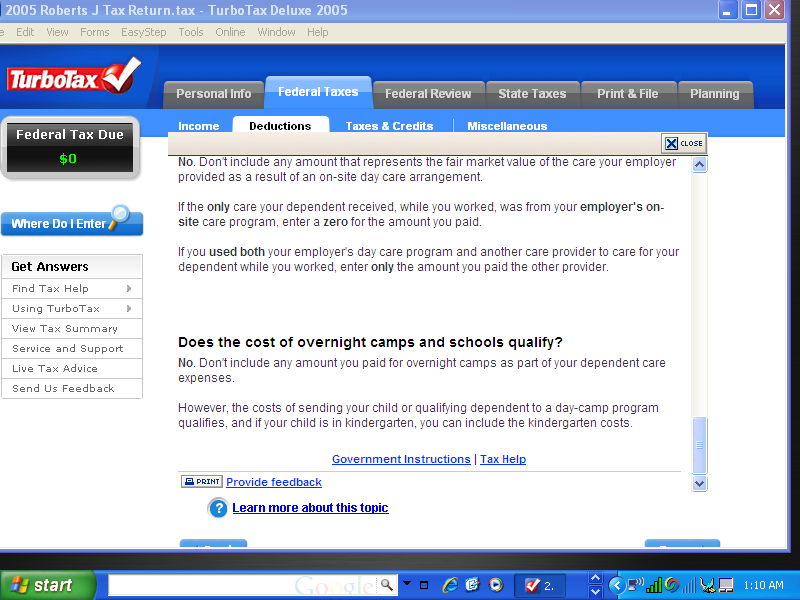

If, however, you click the button "Learn more about this topic," then you see a small number of questions and answers, the last of which clearly states that overnight camps do not qualify for the credit. Accordingly, if Geithner were curious about whether these camp expenses qualified, one of the two links he might have clicked would have given him an answer.

Screenshot from 2005 TurboTax

(click once to open, and then again to read)

Again, while TurboTax did not make a "mistake," TurboTax would not have prompted Geithner specifically about the overnight summer camp. This time, however, the link "Learn more about this topic" would have supplied the correct answer. But if he didn't click on this link, TurboTax would not have informed Geithner that overnight camp didn't qualify for the child care credit.

CONCLUSION:

Contrary to the comments of some on the web (via Instapundit), neither of the two major errors in Geithner's returns that I explored would have been covered by interactive prompts in the 2004 or 2005 versions of TurboTax.

Other tax issues, which I am not commenting on, include these:

1. Geithner's failing to refile in 2006 and pay back self-employment taxes from 2001 and 2002 after he was audited on that issue for the 2003 and 2004 tax years. He waited until he was nominated to head up Treasury to pay these taxes that the IRS could no longer demand because of the statute of limitations.

2. Geithner's failing to refile and pay back tax credits for overnight camp in 2001, 2004, and 2005, when he was informed in 2007 (or 2006) by an accountant that his credit for overnight camp was not allowed. Apparently, in 2007 the 2004 and 2005 returns were not quieted by the statute of limitations, though the 2004 return had been previously audited by the IRS.

3. Geithner's failing to report and pay a 10% penalty on an early withdrawal from a government pension.