Secret Tapes of George W. Bush:

An interesting piece in today's New York Times.

Saturday, February 19, 2005

Horse and Buggies Versus Cars:

Is it possible to write a lengthy article on the safety and other risks posed to consumers by early automobiles, have it reviewed by prominent legal historians, and published in a prestigious legal history journal, without ever considering the issue as to whether cars were more or less safe than the horse and buggies they substituted for? (Aside: one of my great-grandfathers was killed in a horse and buggy accident.) Even if one of the primary cases you focus on involved a defective wheel, an issue that no doubt arose with regard to buggies/carriages as well?

Not only is it possible, it's been done. The same article manages not to ignore the abundant law and economics scholarship on consumer warranties, but rather to only cite the few L & E scholarship (Logue, Hanson, Croley) who are sympathetic to enterprise liability. Friedrich Kessler, of contracts of adhesion fame, is cited often, but George Priest (among others who have harshly criticized Kessler) is cited not once. As someone who does a lot of work in legal history, this sort of thing frustrates me quite a lot.

Friday, February 18, 2005

When Barry Lynn Speaks, Tony Mauro Listens:

Tony Mauro has a new article in Legal Times that begins:

This seemed like a pretty tenuous connection to me, so I re-read the article to find out who the people are that find this controversial. As best I can tell, the article's only source for that view is a single man: Barry Lynn, the executive director of Americans United for Separation of Church and State. I think it's fair to describe Lynn as a harsh and regular critic of Justice Thomas. Come to think of it, I don't think I've ever seen Lynn make a comment about Justice Thomas that wasn't harshly critical. Maybe it has happened, but if it has it would be, well, pretty newsworthy.

Here's my question: Is the fact that Barry Lynn objects to something Justice Thomas did itself worthy of a news story? Perhaps lots of people see the fact that Justice Thomas would swear in a protege of Roy Moore as controversial, and Mauro just chose Lynn to quote as representative of that view. Perhaps there is something else to this story that was cut out during the editing process. But the story as written seems to be about Barry Lynn's objections, and only his objections. Maybe I'm missing something, but this story seems to be less about reporting on a controversy than trying to create one.

UDPATE: While it doesn't have anything to do with Lynn's rationale for criticizing Thomas, this important post over at Southern Appeal is more than enough to convince me that that Parker is someone Justice Thomas shouldn't be supporting. Oddly, it may be that swearing in Parker should be controversial — just not for the reasons Mauro mentions in his article.

Justice Thomas Finds Himself in Inauguration ControversyAccording to the article, the private swearing in of Justice Parker generated "some controversy" because Justice Paker is a protege of Alabama Chief Justice Roy Moore, the so-called "Ten Commandments judge," who defied the federal courts by refusing to comply with judicial orders to remove the Ten Commandments from the courthouse that hosts the Alabama Supreme Court. The controversial part about swearing in Parker, according to Mauro, is that the Supreme Court will be deciding cases this Term on the constitutionality of Ten Commandment displays. The article suggests that offering symbolic support to someone who is a close friend of someone closely associated with the public debate over issues relating to a pending case is problematic, even if the support was private.

Tony Mauro

Legal Times

02-17-2005

A week before Supreme Court Chief Justice William Rehnquist swore in President George W. Bush to a second term as president last month, Justice Clarence Thomas presided over a little-noticed inauguration inside the Court building that has generated some controversy.

In an invitation-only ceremony, Thomas on Jan. 13 gave the oath of office to newly elected Alabama Supreme Court Justice Tom Parker. . . .

This seemed like a pretty tenuous connection to me, so I re-read the article to find out who the people are that find this controversial. As best I can tell, the article's only source for that view is a single man: Barry Lynn, the executive director of Americans United for Separation of Church and State. I think it's fair to describe Lynn as a harsh and regular critic of Justice Thomas. Come to think of it, I don't think I've ever seen Lynn make a comment about Justice Thomas that wasn't harshly critical. Maybe it has happened, but if it has it would be, well, pretty newsworthy.

Here's my question: Is the fact that Barry Lynn objects to something Justice Thomas did itself worthy of a news story? Perhaps lots of people see the fact that Justice Thomas would swear in a protege of Roy Moore as controversial, and Mauro just chose Lynn to quote as representative of that view. Perhaps there is something else to this story that was cut out during the editing process. But the story as written seems to be about Barry Lynn's objections, and only his objections. Maybe I'm missing something, but this story seems to be less about reporting on a controversy than trying to create one.

UDPATE: While it doesn't have anything to do with Lynn's rationale for criticizing Thomas, this important post over at Southern Appeal is more than enough to convince me that that Parker is someone Justice Thomas shouldn't be supporting. Oddly, it may be that swearing in Parker should be controversial — just not for the reasons Mauro mentions in his article.

Term Limiting Supreme Court Justices:

Lately I was asked to endorse the following proposal by law professors Paul D. Carrington and Roger C. Cramton to limit the terms of Supreme Court Justices:

I tend to favor term limits--what the Founders called "rotation in office"--for elected officials, but this proposal gave me pause. I am not as unhappy with the current system of judicial appointments as some on the left and right. Still, this proposal seems to have some merits in that it regularizes the process of adding new members to the court. (I cannot find the actual proposal on line so you can read the justifications offered by its authors, but you can read a New York Times story on the proposal here. If someone finds a link to the full proposal, I will add it here.)

So far, I have not signed on, but was curious to hear thoughtful reader reaction. So I have activated comments. I am particularly interested in hearing potential problems with the proposal, as its purported benefits are more obvious. However, feel free to voice your support as well as opposition. But reasons will be more persuasive to me than expressed preferences.

THE SUPREME COURT RENEWAL ACT OF 2005As explain by its authors, this proposal would have the effect of limiting the term of "active" justices to approximately 18 years:

Congress should enact the following as section 1 of Title 28 of the United States Code:

(a) The Supreme Court shall be a Court of nine Justices, one of whom shall be appointed as Chief Justice, and any six of whom shall constitute a quorum.

(b) One Justice or Chief Justice, and only one, shall be appointed during each term of Congress, unless during that term an appointment is required by Subsection (c). If an appointment under this Subsection results in the availability of more than nine Justices, the nine who are junior in commission shall sit regularly on the Court. Justices who are not among the nine junior in commission shall become Senior Justices who shall participate in the Court's authority to adopt procedural rules and perform judicial duties in their respective circuits or as otherwise designated by the Chief Justice.

(c) If a vacancy occurs among the nine sitting Justices, the Chief Justice shall fill any temporary vacancy by recalling Senior Justices in reverse order of seniority. If no Senior Justice is available, a new Justice or Chief Justice shall be appointed and considered as the Justice required to be appointed during that term of Congress. If more than one such vacancy arises, any additional appointment will be considered as the Justice required to be appointed during the next term of Congress for which no appointment has yet been made.

(d) If recusal or temporary disability prevents a sitting Justice from participating in a case being heard on the merits, the Chief Justice shall recall Senior Justices in reverse order of seniority to provide a nine-member Court in any such case.

(e) Justices sitting on the Court at the time of this enactment shall be permitted to sit regularly on the Court until their retirement, death, removal or voluntary acceptance of status as a Senior Justice.

The result is that all Justices appointed to the Court in the future would serve as the nine deliberating and deciding members for a period of about eighteen years (depending upon the interval between the initial appointment and the promptness of the appointment process eighteen years later). However, the Act does not restrict the lifetime tenure of the Article III judges appointed as a Justice or Chief Justice of the Supreme Court. Instead, it defines the regular membership of the Court as consisting of the nine most recently appointed Justices. Some of the Senior Justices who no longer participate regularly in the Court's decisional work may be called upon to provide a nine-member Court when that is necessary (see Subsection (d)). And all of them continue to retain the title of "Justice of the Supreme Court" and to exercise the judicial power of the United States as judges of a circuit court, a district court, or some other Article III court. In short, the Act defines the "office" of a Supreme Court "judge" in a new way. This feature distinguishes the Act from statutory proposals to place age limits or fixed terms of service on Supreme Court Justices. Senior Justices will continue to have lifetime tenure as Article III judges in accordance with the "good behavior" clause of Section 3 of Article III.This proposal has already been endorsed by law professors representing a wide political spectrum. They include: Vickram D. Amar, Jack M. Balkin, Steven G. Calabresi, Walter E. Dellinger III, Richard A. Epstein, John H. Garvey, Lino A. Graglia, Michael Heise, Yale Kamisar, and Sanford Levinson.

I tend to favor term limits--what the Founders called "rotation in office"--for elected officials, but this proposal gave me pause. I am not as unhappy with the current system of judicial appointments as some on the left and right. Still, this proposal seems to have some merits in that it regularizes the process of adding new members to the court. (I cannot find the actual proposal on line so you can read the justifications offered by its authors, but you can read a New York Times story on the proposal here. If someone finds a link to the full proposal, I will add it here.)

So far, I have not signed on, but was curious to hear thoughtful reader reaction. So I have activated comments. I am particularly interested in hearing potential problems with the proposal, as its purported benefits are more obvious. However, feel free to voice your support as well as opposition. But reasons will be more persuasive to me than expressed preferences.

Update: On comments, Crime and Federalism Blog notes this online Legal Affairs Debate last week between Norman Ornstein of AEI and my BU colleague Ward Farnsworth. Readers may want to read it before adding their 2 cents.

Related Posts (on one page):

- A CLOSER LOOK AT TERM LIMITS; PROBLEMS WITH THE CARRINGTON/CRAMTON PROPOSAL.�

- Term Limiting Supreme Court Justices:

- NY Times article on Supreme Court term limits.--

Summers Transcript Released:

Harvard has released a transcript of the remarks by President Lawrence Summers that has gotten him into such hot water. You can access them here.

Journal Name Change:

This may be just a coincidence, but only a few weeks after Harvard President Lawrence Summers' controversial remarks on possible innate differences between men and women, the Harvard Women's Law Journal has decided to change its name to the Harvard Journal of Law & Gender. In a letter to the editor of the Harvard Law Record, the editors-in-chief of the Journal explain that the name change "indicates our unwillingness to rely upon essentialist arguments based on biological sex," among other things. Of course, if this change was in fact triggered by Summers' speech, it pales in comparison to other fallout from the speech.

IMAO Group-Blogging:

IMAO, formerly Frank J.'s private preserve, has become a group blog (announcement here). The e-mail informed me that, "IMAO will surely now storm to the top of the blogosphere, leaving many bodies in its wake. Pity IMAO's enemies."

Also, the e-mail included a note: "Your link to IMAO has the site's name spelled wrong (it's 'IMAO' not 'Scrappleface'). Also, the URL is all wrong."

New Mexico Lesbian Devil Sex Case:

I blogged about this prosecution earlier this week; my view was that the accused simply wasn't guilty of a crime under New Mexico law, at least under that portion of New Mexico law -- distribution to minors or display to minors of obscene-as-to-minors materials -- that was being discussed.

Ruth Waytz, the wife of the artist who drew the allegedly obscene-as-to-minors sticker, now reports:

Dean Young's case was dismissed this morning, but the judge did so Without Prejudice, which means the NM authorities are still free to file other charges against him in the future. Not sure what those other charges might be . . . .

Maybe Young did something else that actually was a crime, but my sense is that he's off the hook for the sticker.

Related Posts (on one page):

- New Mexico Lesbian Devil Sex Case:

- New Mexico Sticker Case:

"History Doesn't Repeat Itself, But It Rhymes":

A while back, I got several messages from readers attributing this quote to Mark Twain. I'm always skeptical of such attributions, since Twain -- plus a few other people, such as Winston Churchill, Dorothy Parker, George Bernard Shaw, Oscar Wilde, Ambrose Bierce, Benjamin Disraeli, and H.L. Mencken -- seem to be magnets for loose quotations. If you're not sure of the source, credit Twain, and that'll be plausible enough. So I asked the indispensable UCLA Law School research library to track it down. (Yes, I can legitimately do that, since I plan on using the quote in my law review article.)

Here's what seems to be the scoop, courtesy of Jenny Lentz: The quote has indeed been often attributed to Mark Twain, but there doesn't seem to be much proof that he indeed said it. The most detailed source she could find was this note in an article by Lawrence P. Wilkins in 28 Indiana Law Review 135 (1995):

[The quote was a]ttributed [to mark Twain] by Allen D. Boyer in Activist Shareholders, Corporate Directors, and Institutional Investment: Some Lessons from the Robber Barons, 50 WASH. & LEE L. REV. 977, 977 (1993), who saw the attribution in ROBERT SOBEL, PANIC ON WALL STREET 431 (1988). Professor Sobel saw the attribution some time ago in an editorial column in the New York Times, the author of which he cannot recall. He has consulted with several Twain scholars across the country, and all agree that the quotation sounds very much like something Twain would say, but none seems able to find the actual words in Twain's papers. Telephone conversations with Allen D. Boyer and Robert Sobel, March 3, 1995 and March 7, 1995. It is somewhat ironic that this quotation cannot be definitively traced to Twain, whose energies were spent in great measure to protect his rights of authorship. . . .

In any case, I can still easily use the quote, just giving it as "Attributed to Mark Twain." But it's worth noting that there's some uncertainty about it. If anyone can resolve this uncertainty by a specific pointer to a written work by Twain -- and not just by a pointer to someone who has attributed the quote to Twain -- please let me know.

Talk About No Respect...

This from the the Manhattan Jaspers basketball website:

Manhattan gets back in action on Saturday, February 19, when the Jaspers travel to Fairfax, VA to take on George Washington in the team's final non-conference game. Tip-off is slated for 4:00 p.m.

GMU beat 23-3 Old Dominion, earns an ESPN Bracket Buster game this weekend, and the team they are playing still can't get the name right. It is George Mason, not George Washington, and not Georgetown! Its bad enough being the other "George" school around here, but sometimes it gets old being the other, other "George" school in these parts.

Related Posts (on one page):

- Ha! I'll Bet They Know Who We Are Now!

- Talk About No Respect...

Thursday, February 17, 2005

The Shape of Bloggs:

I thought about this while reading to Benjamin, but of course great minds think alike.

Yet Another Ridiculous Lawsuit:

Ted Frank (OverLawyered) reports:

Michael J. Zwebner, the CEO of penny-stock holding company Universal Communication Systems, is unhappy that he's being flamed on the RagingBull.com message board, run by Lycos. He may have a legitimate beef to some extent. . . .

[But] Zwebner's litigation methods . . .are questionable. He's filed five lawsuits in federal court in Miami, against anonymous posters, against Lycos (for, among other things, "trademark violations" for naming a message board after the ticker symbol UCSY), and even a couple of purported class actions. He's especially upset at one anonymous poster, who has the especially credible username of Wolfblitzzer0 [sic].

So, Zwebner has sued . . . CNN and the real-life Wolf Blitzer! It seems, according to Zwebner's view of the world, that Blitzer is supposed to be on the lookout for anonymous posters using similar names, and should be held liable for such posters' postings when he fails to police the use of such usernames. . . .

Appalling. First, I doubt that Blitzer even had a legal right to stop Wolfblitzzer0 from his posts; unless the posts were commercial advertising (which I doubt), Blitzer wouldn't have a right of publicity or trademark claim against Wolfblitzzer0. And I doubt Blitzer would have a libel claim (on the theory that Wolfblitzzer0 is hurting Blitzer's reputation by posting things under his name) because few readers would really think that the poster is Wolf Blitzer.

But second, Blitzer certainly has no legal duty to spend his time, money, and effort litigating over every schmoe's misuse of his name -- even if he had a legal right to stop such misuses -- especially when readers would realize that the poster isn't the real Blitzer. (Under the doctrine of "apparent authority," A may sometimes end up bound by contracts that B made on his behalf, when reasonable observers would assume that B actually has the authority to act for A; but that surely isn't the case here.)

Sounds like a sure loser of a case to me, perhaps even sanctionable (though that's a tougher call).

Eric Muller on Thomas Woods's "Politically Incorrect Guide to American History":

I thought I'd blogged Eric's views on this when he first posted them, but now I realize I hadn't. In any case, they start here, but he has a lot more follow-up. Max Boot's piece, which I linked to below, properly gives Eric credit.

Kyoto Comes into Force:

Yesterday the Kyoto Protocol to the United Nations Framework Convention on Climate Change — aka the UN global warming treaty — came into effect. This became a done deal after Russia agreed to ratify the agreement. By its terms, Kyoto enters into force on the 90th day after at least 55 countries representing at least 55 percent of global carbon dioxide emissions in 1990 ratify the agreement.

Contrary to some claims, the U.S. never "withdrew" from Kyoto the way it withdrew from the International Criminal Court. The U.S. remains a party. Nonetheless, this nation is not bound by its terms because the U.S. has not ratified it. Most other developed nations have ratified Kyoto, however, and are bound by its terms — at least in theory. Many of Kyoto's signatories in Europe are well behind their emission reduction goals, and developing nations are not required to reduce their emissions at all. As Julian Ku notes at Opinio Juris, many Kyoto signatories are heading in the "wrong direction."

The Bush Administration has been the subject of substantial criticism for refusing to endorse Kyoto. But is this criticism warranted? The Clinton Administration signed the treaty, but never submitted it to the Senate for ratification. The Senate passed the Byrd-Hagel Resolution 95-0, unanimously rejecting the substance of the agreement. Even some who believe global warming is a pressing policy concern doubt Kyoto represents a responsible strategy to address climate change concerns.

The underlying assumption of much anti-Bush Kyoto commentary is that the Bush Administration is doing nothing on the issue. Even if one sets aside the tens of millions the administration has spent on climate-related research and technology R&D on the assumption that such federal projects rarely bear fruit, the charge that the Administration is sitting on its hands rings hollow. As Gregg Easterbrook notes in The New Republic, the Administration's "Methane to Markets" initiative represents a substantial step toward reducing greenhouse gas emissions. (For non-TNR-subscribers, Julian Ku summarizes the article here.) While few have noticed this program, it could do as much to reduce the threat of global warming as Kyoto as methane is a more potent greenhouse gas than CO2.

Despite its promise, I would not expect too many environmental activists to cheer "Methane to Markets." First, as we have seen in other contexts (see here and here), the major environmental groups are loathe to give a conservative Republican administration much credit for any environmental initiatives. Second, although "Methane to Markets" could bear fruit, it does not require stringent regulations of coal-fired power plants, limitations on fossil fuels, or controls on SUVs. Third, as Ku suggests, there is often a preference for grand international agreements (like Kyoto) over less-formal — but not necessarily less-effective — agreements like "Methane to Markets." It will be interesting to see whether this agreement is a one-shot deal, or a harbringer of more to come.

Chart on Attorney Advertising and Bankruptcy:

I have a very busy day, so I don't have time for another long post on bankruptcy reform (I'll get back to it tomorrow I hope if I have time), so I'll just leave you with a self-explanatory chart on trends on attorney advertising and bankruptcy filings that is contained in my latest article:

Numerous caveats apply--this is just tv, it is all advertising and not just for bankruptcy, etc. So I'll just let you make of this what you wish and leave it at that.

Update:

2 points. First, I made no claim about causation in my original posting--there could be no causal link at all here and if there is correlation, it could be spurious. If there is a causal link, it could run in either direction (e.g., public demand for bankruptcy lawyers could lead to more advertising). Second, there is a very well established empirical literature that advertising for legal services increases demand for legal services, so that the relationship is theoretically possible, unlike, for instance, other random correlations that some have drummed up. I thought the underlying model was obvious, but apparently some who criticized me weren't aware of this vast body of academic literature. And, of course, there is other empirical evidence that finds some sort of relationship between lawyer advertising and bankruptcy filings, although again, existence and direction of causation remain open. Whether this particular chart provides any additional empirical evidence or intuition to support the theory, as I said once already, I leave to you. But that doesn't mean the theory doesn't make any sense.

Wednesday, February 16, 2005

Monday's Talk at Quinnipiac:

Although it is not yet on their website, my talk on Monday (2/21) on Ashcroft v. Raich at Quinnipiac University School of Law has been scheduled for noon in the Grand Courtroom. The event is open to the public.

Also next week, I will be speaking at Cumberland Law School Birmingham AL (noon - 2/24) and at the University of Alabama School of Law in Tuscaloosa (noon - 2/25).

Also next week, I will be speaking at Cumberland Law School Birmingham AL (noon - 2/24) and at the University of Alabama School of Law in Tuscaloosa (noon - 2/25).

Related Posts (on one page):

- Monday's Talk at Quinnipiac:

- Corrected Speaking Times:

- Speeches This Week

Forward-Thinking Universities:

I just noticed that a university other than UC was smart enough to snag uc.edu before UC did. Likewise, I've long noticed that one particular school is law.edu. If anyone has other examples of universities that have such domain names -- names that do match the school's name or field, but that seem to reflect the school's wisdom in being first to snag a name that other more prominent schools might have also wanted -- please leave them in the comments.

Interesting Star Trek Initiative (UPDATE: NEVER MIND):

A reader just passed along to me this link to an interesting posting by J. Michael Straczynski, the creator of Babylon 5. (Volokh readers have much praised Babylon 5 to me but I could never get into it during its first run.) After a discussion of how the Star Trek franchise evolved to this point, here is how it provocatively ends:

Last year, Bryce [Zabel (recently the head of the Television Academy and creator/executive producer of Dark Skies)] and I sat down and, on our own, out of a sheer love of Trek as it was and should be, wrote a series bible/treatment for a return to the roots of Trek. To re-boot the Trek universe.

Understand: writer/producers in TV just don't do that sort of thing on their own, everybody always insists on doing it for vast sums of money.

We did it entirely on our own, setting aside other, paying deadlines out of our passion for the series. We set out a full five-year arc.

But when it came time to bring it to Paramount, despite my track record and Bryce's enormous and skillful record as a writer/producer, the effort stalled out because of "political considerations," which was explained to us as not wishing to offend the powers that be.

So on behalf of myself and Bryce, I'm taking the unusual step of going right to the source...right to you guys, fueled in part by a number of recent articles and polls, including one at www.scifi.com/scifiwire in which nearly 18,000 fans voted their preference for a new Trek series,

and 48% of that figure called for a jms take on Trek. (The other choices polled at about 18% or thereabouts.)

See, if somebody doesn't like a story, doesn't want to buy it, that's all well and good, that's terrific, that's the way it's supposed to be.

But when "political considerations" are the basis...that just doesn't parse.

So here's the deal, folks. If you want to see a new Trek series that's true to Gene's original creation, helmed by myself and Bryce, with challenging stories, contemporary themes, solid extrapolation, and the infusion of some of our best and brightest SF prose writers, then you need to let the folks at Paramount know that. If the 48% of the 18,000

folks who voted at scifi.com sent those sentiments to Paramount...there'd be a new series in the works tomorrow.

I don't need the work, I have plenty of stuff on my plate through 2007 in TV, film and comics, so that's not an issue. But I'd set it all aside for one shot at doing Trek right, and I know Bryce feels the same.

Update: NEVER MIND! Here is a follow up post from J. Michael Straczynski:

Actually...belay everything I just said.Well, THAT was fast!

In the 24 hours between the time I composed the prior note, and sent it, and it made its way through the moderation software, two things happened:

1) I heard from a trusted source that Paramount is giving the Trek TV world a rest for maybe one to two years, depending on circumstances, no matter who would come along to run it. So it's not right to have folks putting in time doing something that ultimately would be pointless, I don't think that's a proper use of anybody's time.

2) At the same time as the above, an offer came in to run a new TV series for fall of '06, and since there's no way anything Trek can happen in the interim, I've said yes (now we have to negotiate the deal, but that should be fairly straightforward).

So on two counts, the whole thing is kind of moot.

We can reconvene a year or two down the road to see where this takes us, but in the interim...my apologies for waking everybody up in the middle of the night.

As you were.

Related Posts (on one page):

- Interesting Star Trek Initiative (UPDATE: NEVER MIND):

- " 'Dja Get That? "

- Bloggers v. Journalists:

- The Joy of Blogging & More on Startrek Enterprise:

- Star Trek Enterprise Cancelled:

New Daily Feature on NRO:

In addition to The Corner and TKS (formerly "The Kerry Spot"), National Review Online is now offering the Beltway Buzz. Here is its introduction:

Welcome to Beltway Buzz

02/15 01:10 PM

We're constantly thinking of new ways to make NRO bigger and better. With that general goal in mind, today National Review Online introduces a new feature: "Beltway Buzz," which promises to be required reading for anyone looking for Washington, D.C.-focused news and analysis.

We're delighted to have Eric Pfeiffer, formerly of National Journal's sweet daily political candy, "The Hotline," on board to be your daily Beltway buzzer. Welcome, Eric and welcome new Beltway Buzz bookmarkers. Enjoy.

— Kathryn Jean Lopez, Editor, National Review Online

Here It Begins

02/15 01:13 PM

Welcome. I'm Eric Pfeiffer and I'll be your Buzz guy.

This page is now home to a daily feature that aims to provide readers with a fresh look at news and analysis from inside Washington.

First, a little background on me: For the past three years I wrote for "The Hotline," a daily political briefing published by the National Journal. While at "The Hotline," I contributed articles regularly to NRO, The Weekly Standard, the Americas Future Foundation, and others. Early risers can also find me occasionally offering weekly political analysis with ABC News Now.

My main focus here is to provide readers with a fresh angle on political news: the story behind the story you get on the evening news, the counter-story to the conventional wisdom of the day, etc. The Beltway Buzz will be a filter for anyone who wants to be in the know. And it will break some news, too.

And we're on the Internet, so feedback is easy to provide and is encouraged. My e-mail is efeiffer@nationalreview.com — so you know where to find me.

Thomas Woods's "Politically Incorrect Guide to American History":

Max Boot (not a particularly politically correct fellow himself, writing in the not very politically correct Weekly Standard) criticizes it forcefully and in detail.

Boot also points out the error in the New York Times Book Review's characterization of the book as a "neocon retelling of this nation's back story," faults Regnery, Woods' publisher, and warns conservative consumers: "Conservatives looking to inoculate themselves or their children from liberal indoctrination would be well advised to steer clear of Woods's corrosive cornucopia of canards."

Related Posts (on one page):

- Eric Muller on Thomas Woods's "Politically Incorrect Guide to American History":

- Thomas Woods's "Politically Incorrect Guide to American History":

Good for You:

First alcohol, now coffee (though unfortunately maybe decaf is best).

Of course, "That difference may, however, be due to differences in lifestyle, the researchers commented, suggesting that drinkers of decaffeinated coffee might be more health-conscious overall." But, hey, I know how to ignore scientific disclaimers just as well as the next guy.

New Study on Dynasty Trusts and the Abolition of the Rule v. Perpetuities.--

The Wall Street Journal has a story today on a pathbreaking new study just completed by two of my brilliant young Northwestern colleagues, Rob Sitkoff and Max Schanzenbach. Unfortunately, the Journal's article is available only to subscribers, but the Journal's story is already up on Westlaw (2005 WL-WSJ 59841238) for academics who have that subscription.

The study (which can be freely downloaded from SSRN) examines whether trust assets are moving into states that repealed the Rule v. Perpetuities and thus permit perpetual dynasty trusts. Rachel Silverman in the Journal explains:

Until recently, trusts could effectively last only about 90 to 120 years, under a law called the Rule Against Perpetuities. Since the mid-1990s, a growing number of states moved to relax the term limits. Now, at least 18 states and jurisdictions — including Delaware, Wisconsin, New Jersey, Illinois, Virginia and the District of Columbia — allow trusts to last forever. Several states that impose term limits allow much longer durations. Wyoming and Utah, for instance, permit trusts to last 1,000 years, while Florida lets them carry on for 360 years.

To set up a dynasty trust, it isn't necessary for families to live in a state that permits them. Only a trustee has to be located there — and many trust companies have operations in Delaware, Florida or other states that welcome long-term trusts. Moreover, some of those states, such as Alaska, have other trust-friendly benefits, like no state income taxes on trusts and strong asset-protection laws.

The study found that simply changing a state's perpetuities laws wasn't enough to attract trust assets. Whether a state levied income tax on trust funds mattered, too. If a state abolished its rule against perpetuities, but still taxed trust funds attracted from out of state, the researchers found "no observable increase" on a state's reported trust assets. By contrast, if a state allowed dynasty trusts but also didn't tax trust funds created by nonresidents, the state's reported trust assets increased by roughly $13 billion on average during the time period studied.

The study finds that a lot of trust money has been flowing into South Dakota, Delaware, and Illinois (among others)--states that repealed the Rule v. Perpetuities and have no fiduciary income tax on trusts holding assets for out-of-state beneficiaries.

Here is the abstract to the scholarly paper:

Jurisdictional Competition for Trust Funds: An Empirical Analysis of Perpetuities and Taxes

This paper presents the first empirical study of the jurisdictional competition for trust funds. In order to open a loophole in the federal estate tax, a rash of states have abolished the Rule against Perpetuities. Based on reports to federal banking authorities, we find that through 2003 a state's abolition of the Rule increased its trust assets by $6 billion (a 20% increase on average) and increased its average trust account size by $200,000. These estimates indicate that roughly $100 billion in trust funds have moved to take advantage of the abolition of the Rule. Interestingly, states that levied an income tax on trust funds attracted from out of state experienced no increase in trust business from abolishing the Rule. This is a striking finding for the theory of jurisdictional competition, because it implies that abolishing the Rule does not directly increase a state's tax revenue. These results also have relevance for theories relating to altruism and the bequest motive. The main tax benefits of establishing a perpetual trust accrue not to the donor or anyone she knows, but to beneficiaries whom the donor has never met - the unborn.

The study will be important to academics because it is the first major empirical paper on the competition among states for trust business. Academics know that there is a massive empirical literature in corporate law on state competition for corporate charters, but (until now) there has not been a similar literature in Trusts & Estates.

Sitkoff and Schanzenbach's conclusion: If you build it, they will come.

Hot tip for any law review editors reading this blog: Check your mailboxes over the next few weeks; in its field this article will be a blockbuster.

FTC Study on On-Line Sales of Replacement Contact Lenses:

Important new study of competition and consumer protection issues involving on-line sales of replacement contact lenses can be found here.

Great example of how the FTC can use its research tools to advance understanding of market competition furthers consumer welfare and how wrongheaded professional licensing requirements can harm consumers.

The Other Bankruptcy Blogger:

Apparently there are two of us now who blog on bankruptcy issues. For those who prefer a "front lines" analysis (and a bit more "colorful" take) rather than my academic analysis of bankruptcy reform, see the State 29 blog.

With 2 of us, I think that pretty much satiates the public's appetite for bankruptcy-related blogs.

Update:

Whoops, Kemplog points out that I missed one--Automatic Say. So there are three of us--soon we will overtake all those Constitutional Law blogs out there!

Health Problems and Bankruptcy--Are 50% of Bankruptcies Health Related?:

In Senate testimony last week, one of those testifying offered the observation, "One million men and women each year are turning to bankruptcy in the aftermath of a serious medical problem—and three-quarters of them have health insurance." In a column in the Washington Post last week, Professor Elizabeth Warren (who also gave the just quoted testimony) stated, "[H]alf [of bankruptcy filers] said that illness or medical bills drove them to bankruptcy," an assertion that was repeated at the Hearings last week on the bankruptcy reform legislation. Most of the Democratic Senators in attendance accepted the assertion that 50% of bankruptcies are caused by health problems without question (even going so far as to silence me when I raised doubts about the credibility of that figure). It has also been widely reported in the media.

Professor Warren writes, "With the dramatic rise in medical bankruptcies now documented, this tired approach would be no different than a congressional demand to close hospitals in response to a flu epidemic." This figure was used to throw cold water on the bankruptcy reform legislation, and it is expected that Sen. Feinstein at least will propose an amendment.

But is it true that it is "now documented" that 50% of bankruptcies are caused by health problems?

The conclusion is based on a study in Health Affairs. Reviewing the study, it appears that the estimate that 50% of bankruptcy filings are precipitated by a "serious medical problem" cannot be supported based on what that study actually examined.

First, the study comes on the heels of many studies over many decades that find mixed evidence for the belief that a substantial number of consumer bankruptcies are caused by health problems. Those that did find some relationship often found a very small relationship, which explains why Professor Warren has described it as "a dramatic rise" in medical bankruptcies. For instance, in an earlier book, Professor Warren and co-authors wrote, "The central finding is that medical debt is not an especiallly important burden for most debtors." In a more recent article, it was observed that "until the 1990s . . . most empirical studies of bankruptcy did not find illness, injury, or medical debt to be a major cause of bankruptcy." Indeed, in the Health Affairs article, it is stated that medical bankruptcies increased 23-fold over the past two decades. No previous credible study has ever found anything approximating the conclusion that 50% of bankruptcies are caused by medical problems. The appearance of such a huge anomaly usually augurs caution in interpreting the results in light of the massive contrary results on the other side. Such caution is warranted here.

In fact, the "finding" in this article of a massive rise in medical bankruptcies appears to actually be a result in the way in which medical bankruptcies are counted, rather than an actual change in the numbers. They draw their data from two sources. First, self-identified bankruptcy filers who say that some medical event "caused" their bankruptcy. Second, analysis of "objective" facts on filers bankruptcy papers that find either (1) debtor or spouse lost at least 2 weeks of work-related income because of illness or injury or (2) uncovered medical bills exceeding $1,000 in 2 years before bankruptcy, or (3) debtors who say they had to mortgage their home to pay medical bills (which for some reason they list as an "objective" factor rather than a self-identified factor.

Do these findings support the claim that 50% of bankruptcy filings were caused by a "serious medical problem"?

First, consider the self-identified filers. Among the self-identified factors that are listed as "medical" causes of bankruptcy in Exhibit 2 of the article are the following: illness or injury, birth/addition of new family member, death in family, alcohol or drug addiction, uncontrolled gambling. First, it is surely open to question whether uncontrolled gambling or a death in the family really should count as a "medical" problem. More generally, the category "illness or injury" is very broadly defined in the study, and there is no apparent limit on the time frame over which the illness or injury occurred, or the severity. So classifying all of these factors as medical problems that have "caused" bankruptcy certainly seems open to question.

Second, the "objective" measures from the debtors bankruptcy petitions are, if anything, even more questionable. First, the authors count anything above 2 weeks of lost work income as a "serious medical problem." There appears to be no time frame over which this is measured, nor does it apparently even need to be consecutive lost work. So, for instance, if a restaurant waiter called in sick for 2 weeks or more in some indeterminate period of time prior to filing bankruptcy, this would presumably count as a serious medical problem.

Nor does the requirement of $1,000 in unpaid medical bills within 2 years of bankruptcy seem like a very plausible measure of serious financial problems. Again, it is pretty easy to rack up $1,000 in unpaid medical bills over a 2 year period, especially if elective procedures not covered by insurance are added in. Moreover, it is well-understood that debtors who are falling into bankruptcy pick and choose which debts they pay, paying down their mortgage or nondichargeable debts for instance, while not paying their unsecured debts, such as medical and credit card debt. So the fact that the medical debts were unpaid says little, because it may reflect strategic payment of debts prior to bankruptcy.

So the categorization of what counts as a "serious medical problem" is quite questionable in this study. But there is a more fundamental problem that this concern hints at--there is no control group in this study. It is usually Statistics 101 that in order to infer causation from a data observation, it is necessary to have a control group. Absent a control group, it is not clear how the authors can make their claims.

So, for instance, one would want to know how many Americans missed 2 weeks of work or had a $1,000 in medical bills and didn't file bankruptcy. This is precisely why other previous studies have failed to find much of a correlation between health problems and bankruptcy--almost every family in America has a health problem, death in the family, or gives birth every year. Most of them do not file bankruptcy. In short, I suspect a lot of people had medical problems comparable to those who filed bankruptcy, but did not file bankruptcy. Of course, we will never know, because the authors have no control group to determine whether those in bankruptcy were more prone to illness or injury than the population at large.

Moreover, the authors do not compare the amount of medical debt they found to other debt or obligations that bankrupt debtors had. So, for instance, they would count as a medical bankruptcy a debtor who had $1,001 in medical bills, even if that debtor had say $50,000 in student loans, car loans, and other debt. It would be absurd, it seems to me, to say that the $1,001 in medical expenses "caused" that bankruptcy. Nonetheless, it would counted in this study, because the authors do not control for medical debt as a percentage or in relation to the debtors overall debt.

But the problems do not end there. For instance, the authors claim (page W5-71) that from 1981-2001, medical bankruptcies increased 23-fold, citing a study from 1981 published in "As We Forgive Our Debtors." I have read and reread the relevant chapter of that book, and have been unable to determine exactly what criteria were used to classify medical bankruptcies there, and how they compare to here. It appears that the measure used in the earlier work was the pure narrowest form of self-identified filers, those who stated that they filed bankruptcy because of a health problem. In the current study, it appears the authors ask the self-identified filers if health problems were "a reason" for bankruptcy. I can find no evidence that the authors there counted as medical bankruptcies any bankruptcy where the debtor had above a specified amount of medical expenses. Even if it were the case, there is no evidence that the $1,000 figure chosen in the current study was adjusted for inflation over the prior study. Nor is there any indication that the authors attempted to adjust the medical expenses that are found in the current study for increases in debtor's income. So again, it seems like they have just changed their method of counting, not the actual substance.

The authors also do not provide any causal explanation for what could have changed in the medical system to produce a 23-fold increase in health=related bankruptcies in 20 years, and specifically note that the percentage of those in bankruptcy who have health insurance has changed little over that time.

In fact consider the following passage from "As We Forgive Our Debtors":

Our central finding is that crushing medical debt is not the widespread bankruptcy phenomenon that many have supposed. To the extent that the typical debtors in bankrutpcy are painted as sympathetic characters because they are struggling with insurmountable medical debts, these data show that 'typical' is the wrong adjective. Only a few debtors find thmselves in such extreme circumstances.... About half of all debtors carry some medical debt, and many carry substantial medical debt. Althought these medical debts are not the obvious cause of the debtors' bankruptcies they are part of their financial troubles." (p. 173).

Again, what seems to have changed is not the frequency of the underlying problem, but simply the way the data is counted and classified. In the earlier study, the authors noted that half of filers had some amount of medical debt, but recognized that relatively small amounts of unpaid unsecured medical debt or minor injuries were likely not the cause of bankruptcy, because this is a part of the financial life for almost every American family. For the debtors in the earlier study, the medical debt that was found was relatively small in comparison to the bankrupts' other debts. In the more recent study, the authors have simultaneously increased what counts as a "medical problem" and classified even relatively small and trivial medical expenses and problems as bankruptcies "caused" by medical problems. Changing the way you count and classify the same data is not the same thing as finding a 23-fold increase in the underlying problem itself.

I close with an illustration that tries to put the major flaws of this study in perspective and the policy recommendations that have been drawn from it. Suppose that I wanted to find out how many Americans filed bankruptcy because of tax problems. I then interviewed bankruptcy filers and checked their financial records, and counted as a "tax-caused bankruptcy" anyone who either (1) paid $1,000 or more in taxes during the past two years, or (2) anyone who said that if he didn't have to pay taxes he wouldn't have had to file bankruptcy because he would have had more money for his other bills. I suspect that under that criteria I would find a pretty substantial number of "tax-caused bankruptcies." I then conclude that, as a result, we shouldn't make people pay taxes if they believe it might make them file bankruptcy, and that any unpaid tax obligations should get a blanket discharge in bankruptcy (unlike current law, which makes them largely nondischargeable).

Obviously, my hypothetical study of "tax-caused bankruptcies" would be sheer nonsense. I would have no control group (how many other people paid taxes and didn't file bankruptcy), I would have no information about how large my tax payments were relative to other obligations (mortgage, student loans, etc.), and my data would be subject to high rates of self-reporting bias. You would object--"almost everyone pays taxes, what is so unique about this group?" My policy proposal would be ridiculous. In short, my hypothetical study would be properly dismissed as junk science because it fails to use even the most basic statistical controls and techniques.

Let me emphasize--I do not deny that many bankruptcies are caused by health problems. This is why the bankrutpcy reform bill carves out several specific exceptions for treatment of health expenses and health insurance. In theory, the number may be as high as some now say, although as noted, the overwhelming number of studies fail to find anything approximating such a high number. But if it is true, that conclusion cannot be based on this article that is published in Health Affairs that got so much press last week and so much interest in the United States Senate. The statistical classification and methods are just too questionable to support that conclusion.

Tuesday, February 15, 2005

New Mexico Sticker Case:

It turns out that Chris Cooper -- the artist who created that sticker that a New Mexico D.A. says is obscene-as-to-minors -- is a regular reader of this blog (which I hadn't known). He e-mails:

As the artist who created the artwork in question, I'm more than a little interested in this case, and I'm very worried that the person in question might get thrown in the klink for having a sticker on his car. That just doesn't seem like something that should happen in the USA. I hope that your analysis of the statute is one that is shared by the court.

An unsurprising reaction, of course, but I figured that since I had something straight from the horse's mouth, I'd pass it along.

Related Posts (on one page):

- New Mexico Lesbian Devil Sex Case:

- New Mexico Sticker Case:

Newspaper Tries to Intimidate Blogger:

It's hard to gauge the merits without knowing all of the background, but this certainly looks suspicious. (Link via Instapundit)

Constitution-in-Exile:

An organized ideological movement to restore the Constitution-in-Exile finally has begun. Details available here.

UPDATE: Oops!!! I just realized that the site linked to is about inventing a new constitution, not restoring an old one. Obviously that is totally different. My apologies for the error.

UPDATE: Oops!!! I just realized that the site linked to is about inventing a new constitution, not restoring an old one. Obviously that is totally different. My apologies for the error.

Splitting the Proceeds:

Some people asked us how we split our (quite modest) income from this blog. I thought for a while about this. One obvious answer was to pay by the post, but there are obvious bad incentives there. (I doubt that these incentives would affect our judgments consciously, but these things sometimes have a way of subconsciously influencing even well-intentioned people. And I worried about bad incentives for me as much as the bad incentives for others.)

Another was to pay by the total word count, but I don't want people to fall into a "we're getting paid by the word" mentality. We law professors are loquacious enough as it is; no need to encourage us. My sense was that longer posts did tend to be more valuable to readers, up to a certain word count, and excluding block quotes, but not in proportion to their length. I also thought about factoring in the total number of links to our posts, but I decided against this, chiefly because most of our visitors don't come through links to specific posts, and because links end up being hard to measure.

So the formula, which we cobloggers agreed to, is this (and thanks very much to Chris Lansdown of PowerBlogs for implementing the code that supports this): Each person is paid in proportion to the sum of the square roots of their post lengths, with the proviso that the post lengths are in words, exclude blockquoted text, and are capped at 900 words (so one gets no extra credit for words past 900).

My favorite response to this was Dave Kopel's:

Most of all, I'm thrilled to be paid by a system involving the sum of square roots. Maybe I can use the money to buy a slide rule, a pocket protector, and some more black socks.

Yes, the geek chic factor of a sum-of-the-square-roots formula is indeed one of the reasons I chose it . . . .

By the way, no need to suggest alternative schemes; it took us enough time to settle on this one that I doubt we'll reconsider it any time soon.

Whoops!

A New York Times correction from today:

The Keeping Score column in SportsSunday on Jan. 23, about a mathematical formula for projecting the winner of the Super Bowl, misstated the application of the Pythagorean theorem, which the formula resembles. The theorem determines the length of the third side of a right triangle when the length of the two other sides is known; it is not used to determine the sum of the angles in a right triangle.

Thanks to Power Line and InstaPundit for the pointer.

UPDATE: Reader Paul Johnson passes along this Scarecrow line from Wizard of Oz:

The sum of the square roots of any two sides of an isosceles triangle is equal to the square root of the remaining side. Oh joy! Rapture! I got a brain! How can I ever thank you enough?Sounds like the New York Times and the Scarecrow have something in common.

(Note to the New York Times-like among us, or at least those who are NYT-like in this way: The sum of the squares of the two perpendicular sides of a right triangle equals to the square of the remaining side. Remember that the Wizard really didn't improve the Scarecrow's intelligence.)

DC Circuit on Blogging and the Reporter's Privilege:

The DC Circuit has ruled that Judith Miller and Matthew Cooper have no First Amendment privilege not to testify in the Plame investigation, and that if a common law privilege exists it does not apply in their case. In a separate opinion rejecting the notion of a common law privilege, Judge Sentelle pointed out some of the difficulties of applying such a privilege in light of the blogosphere:

Perhaps more to the point today, does the privilege also protect the proprietor of a web log: the stereotypical "blogger" sitting in his pajamas at his personal computer posting on the World Wide Web his best product to inform whoever happens to browse his way? If not, why not? How could one draw a distinction consistent with the court's vision of a broadly granted personal right? If so, then would it not be possible for a government official wishing to engage in the sort of unlawful leaking under investigation in the present controversy to call a trusted friend or a political ally, advise him to set up a web log (which I understand takes about three minutes) and then leak to him under a promise of confidentiality the information which the law forbids the official to disclose?Judge Tatel also wrote separately on the common law privilege question, citing blogfather Eugene's New York Times op-ed along the way. Judge Tatel wrote that he would recognize the privilege, and responded to Sentelle's concern about bloggers by arguing that such distinctions could be drawn on a case-by-case basis:

Nor does it matter that unconventional forms of journalism—freelance writers and internet "bloggers," for example—may raise definitional conundrums down the road. See sep. op. at 5-9 (Sentelle, J., concurring); but see Eugene Volokh, Opinion, You Can Blog, But You Can't Hide, N.Y. Times, Dec. 2, 2004, at A39 ("[T]he rules should be the same for old media and new, professional and amateur. Any journalist's privilege should extend to every journalist."). As Jaffee makes clear, "[a] rule," such as Rule 501, "that authorizes the recognition of new privileges on a case-by-case basis makes it appropriate to define the details of new privileges in a like manner." 518 U.S. at 18. After all, "flexibility and capacity for growth and adaptation is the peculiar boast and excellence of the common law." Hurtado v. California, 110 U.S. 516, 530 (1884). Here, whereas any meaningful reporter privilege must undoubtedly encompass appellants Cooper and Miller, full-time journalists for Time magazine and the New York Times, respectively, future opinions can elaborate more refined contours of the privilege—a task shown to be manageable by the experience of the fifty jurisdictions with statutory or common law protections.

Bankruptcy Reform and Credit Cards:

Naturally, the first question everyone wants to know is isn't the need for bankruptcy reform just a response to "too much" credit card credit. In fact, this argument not only lacks empirical foundation, it lacks sould economic theory to support it.

First, the argument doesn't make much sense from an economic perspective. Unless credit cards have somehow removed the borrowing constraint on individual credit (and no one has provided any evidence that it has), there would be no reason to believe that credit cards would increase overall household indebtedness.

Instead, economic theory would predict that the primary effect of the introduction of credit cars would be to shift around patterns of consumer credit use, by substituting credit card debt for other less-attractive forms of credit, such as pawn shops, personal finance companies, and retail store credit (such as from appliance and furniture stores). In fact, this is what the evidence indicates has actually happened.

Credit cards have not worsened household financial condition, because although consumers have increased their use of credit cards as a borrowing medium, this increase represents primarily a substitution of credit card debt for other high-interest consumer debt. Although this may seem irrational at first glance given the "high" interest rates charged on credit cards, consider that for consumers the alternatives may include pawn shops, personal finance companies, retail store credit, and layaway plans, all of which are either more costly or otherwise less attractive than credit cards.

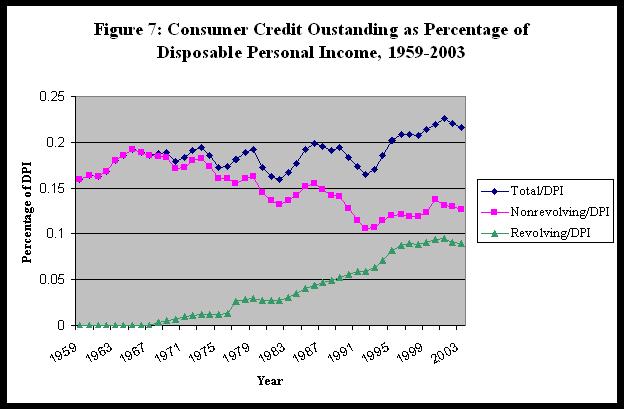

Thus, while credit cards may not be ideal in some absolute terms, their growing popularity reflects the relative attractiveness of credit cards versus these other forms of credit. Credit cards are also generally less expensive for lenders to issue, which is reflected in the overall price of credit cards relative to these other forms of credit. The result, therefore, has not been to increase household indebtedness, but primarily to change the composition of debt within the household credit portfolio. Figure 7, from my article "An Economic Analysis of the Consumer Bankruptcy Crisis" (Forthcoming this year in the Northwestern Law Review) illustrates the nature of this substitution:

Source: Federal Reserve Board and Bureau of Economic Analysis

As this chart indicates, the growth in revolving (credit card) debt has clearly been a substitution from nonrevolving consumer debt to revolving debt, thus leaving overall consumer indebtedness (as a percentage of income) largely unaffected. Revolving debt outstanding has risen during this period from zero to roughly 9% of outstanding debt. Nonrevolving installment debt, by contrast, has fallen from its level of 19% of disposable income in the 1960s, to roughly 12% today. Thus, the increase in revolving debt has been almost exactly offset by a decrease in the installment debt burden. In fact the recent bump in total indebtedness in recent years was not caused by an increase in revolving debt, which has remained largely constant for several years, but by an increase in installment debt, primarily as a result of a recent increase in car loans for the purchase of new automobiles. Thus, there is little indication that increased use of credit cards has precipitated greater financial stress among American households. Because the increase in credit card usage has resulted primarily from a substitution of credit cards for other types of consumer credit, rather than an overall increase in indebtedness.

To the extent that there is some correlation between "high" credit card indebtedness and bankruptcy, but it is questionable whether this supports the causal inference that the credit card debt caused the bankruptcy, rather than the other way around.

First, the correlation between credit cards and bankruptcy may reflect the unique role of credit card borrowing in the downward spiral of a defaulting borrower. Credit cards provide an open line of unsecured credit to be tapped at the discretion of the borrower. Thus, for many debtors credit cards are a "credit line of last resort" to stay afloat to avoid defaulting on other bills. Thus, there may be nothing more than a simple correlation—a debtor confronting a downward spiral may increase his credit card borrowing in the period preceding bankruptcy simply because it is his most easily accessible line of credit. It may appear that because credit card borrowing preceded bankruptcy it also precipitated bankruptcy filing, but if the credit card was being used as a source of credit of last resort, this correlation would not support a causal inference.

Second, a debtor's increased use of credit cards preceding bankruptcy also may reflect strategic behavior taken in anticipation of filing bankruptcy. Credit card debt is unsecured debt that can be discharged in bankruptcy. By contrast, some unsecured debts are not dischargeable in bankruptcy, and secured debts, such as home and auto loans are minimally affected. For unsecured credit card debt, by contrast, generally the debtor can retain the property purchased with the credit card and discharge the obligation. Given the choice between defaulting on secured or nondischargeable obligations on one hand versus dischargeable credit card debt on the other, the incentive is to use credit cards to finance payment of nondischargeable and secured debt. In fact, empirical evidence shows that although credit card defaults have risen in tandem with bankruptcy filings, defaults on secured home and auto loans have remained steady during this period. Debtors also will have an incentive to "load up" their credit card on the eve of bankruptcy, especially by purchasing goods that will not be classified as "luxury goods and services" but might still be quite expensive and the timing of which might be discretionary. Still others simply spend the money or save in exempt assets rather than pay outstanding bills.

One article by Gross and Souleles (cited in my article), for instance find that in the year before bankruptcy, borrowers significantly increase the use of their credit cards, running up their balances rapidly in the period leading up to bankruptcy. This finding is inconsistent with the predictions of the traditional model, which identify credit cards as a special problem because of the gradual, subconscious, and "insidious" manner in which they accumulate over time. If this is true, then the accumulation of credit card debt should be gradual and spread out evenly over time. The rise in credit card debt rises rapidly and is concentrated in the period immediately preceding bankruptcy suggests that credit card indebtedness does not cause bankruptcy in many cases, but that the debtor is already on the way toward bankruptcy when the credit card borrowing begins, and is either acting strategically or is tapping his credit line of last resort.

It also has been argued that credit cards have contributed to increased bankruptcies through a profligate expansion of credit card credit to high-risk borrowers, especially low-income borrowers. Although often-repeated, empirical studies have failed to support this theory. First, the growth in credit card debt by low-income households primarily reflects a substitution for other types of debt, not an overall increase in indebtedness. In addition, two studies have examined the hypothesis empirically and have found little support. The first study, by economists Donald P. Morgan and Ian Toll concludes, "If lenders have become more willing to gamble on credit card loans than on other consumer loans credit card charge-offs should be rising at a faster rate [than non-credit card consumer loans] . . . . Contrary to the supply-side story, charge-offs on other consumer loans have risen at virtually the same rate as credit card charge-offs." Thus "suggest[s] that some other force [other than extension of credit cards to high-risk borrowers] is driving up bad debt."

A second study, by David B. Gross and Nicholas S. Souleles, concludes that changes in the risk-composition of credit card loan portfolios "explain only a small part of the change in default rates [on credit card loans] between 1995 and 1997." Moreover, if it were true that lower-income households were dramatically increasing their indebtedness through credit card increase then this should be reflected in the debt service ratio for lower-income households. As previously noted, however, this ratio has remained largely constant for lower-income households as with all others.

Increasing use of credit cards may be causing higher bankruptcies, but not in the way suggested by critics of reform. Because credit card credit is unsecured, it easily dischargeable in bankruptcy, which may make people more willing to file bankruptcy. Many older forms of credit were secured, such as furniture and appliance credit. Moreover, it may be that people fell less of a personal obligation to repay credit card debt, as opposed credit from a local merchant. But if these explanations explain what is happening, then it seems like this is an argument for bankruptcy reform, rather than against it.

The bottom line is that the standard argument about the relationship between credit cards and bankruptcy does not appear to be consistent with either economic theory or available evidence.

Related Posts (on one page):

- The Poor, Subprime Lending, and the Debt-Service Ratio:

- Debt Service Burden and Consumer Bankruptcies:

- Bankruptcy Reform and Credit Cards:

Lots of Interesting Posts Recently

over at the Conglomerate, including posts on law review membership and visiting professorships. An added bonus: guest-blogging by lawprofs Brett McDonnell and Vic Fleischer in addition to the always-interesting Gordon Smith and Christine Hurt.

Gun Control in the 19th Century South:

My new column for Reason.com explains how the Ku Klux Klan and other racists used gun control in the post-Civil War South to disarm the Freedmen, paving the way for the destruction of their civil rights.

Actors and Politics:

The Thank You, Hollywood, for helping re-elect President Bush billboard made me wonder: Why is it that so many popular and otherwise appealing actors come across so badly -- silly, strident, vacuous, self-important, and the like -- when they talk politics?

Some might say that it's because the actors are silly, strident, vacuous, and self-important. But even if that's right (and I imagine it's true for some and not for others), so what? It's an actor's job to act like someone they're not -- that's what they do for a living. You're not actually a professional baseball player, or an assassin, or the President; but you try to credibly pretend that you are one. Likewise, you may be a pompous ass rather than a thoughtful, empathetic, and trustworthy commentator. But if you're a good actor, you should be able to play thoughtful, empathetic, and trustworthy.

So why don't the actors just treat this as a role? You've got a new gig, which requires a bit of improvising. Your character is someone people trust and like. He's passionate but reasonable, serious but funny, compassionate but hard-headed. He's the guy next door, who's smart enough that his neighbors trust him, but not so full of his smarts that his neighbors loathe him. Your goal is to make the filmgoers like you, and thus like what you say. (Want more incentive? Pretend you're trying to get the Best Actor in a Politically Persuasive Role Oscar. Can't improvise? Heck, don't you know any screenwriters? Have them script some lines for you.)

Does the character call the President dirty names, even when he dislikes him? Does he fail to grasp how patriotic his neighbors are? (Not your real Hollywood neighbors, dummy, the neighbors of the character you're playing.) Does he threaten to move out of the country if the wrong guy gets elected? Seriously, if you're a good actor, shouldn't the answers -- and thus the lines you improvise for yourself -- be obvious?

Heck, if all this doesn't work, here's one for you. Remember Ronald Reagan? Think of him as a great actor? No? Think you could out-act him in your sleep? Think he was evil and hateful, and managed to dupe people into not seeing it? (Never mind that he wasn't, I'll bet you think he was.) Then why could he play amiable, decent, and trustworthy -- even to millions of people who disagreed with him on many things -- and you can't?

Related Posts (on one page):

- Actors and Politics:

- Rubbing It In:

" 'Dja Get That? "

Great final line by Keifer Sutherland on last night's 24. And it wasn't even a season finale like this final line from ST TNG: "Mr. Warf, Fire." Do you have a favorite line from a TV series? I think this will be my last TV blogging for a bit, so I thought I would enable comments (a first for me) to let readers post their favorites. No fair quoting Deadwood. There are probably 15 to 20 good lines per episode.

Update: I don't seem to be able to make comments function. I need to go to class to teach now. Perhaps by the time I get back I will get instructions on how to make this work. I will post another update indicating that comments are working. Sorry for the inconvenience. I do want to hear about other great lines.

Update: COMMENTS NOW WORK!

No Spam and the Joy of Gmail:

I signed up for a Gmail account a while ago, but as I really love the power of Nelson Email Organizer to access my email on Outlook, I had no real use for Gmail. (NEO is amazing! No more folders or filtering. Your Inbox becomes a powerful database.)

The main problem I had with using Outlook and my Treo to access my BU email account was SPAM. I used Mailwasher, a free-standing antispam program designed to strip spam from the server before I download it on Outlook or my Treo, but it has major weaknesses. First it misses a lot of spam (unless you tell it to auto delete all suspected span in which case you risk false positives), and second, it requires my home PC to be running Mailwasher at all times. Sometimes my PC crashes when I am away from home in which case I lose all spam protection.

Since Gmail Now allows downloading your email via a POP3 connection, you can use it with Outlook on your PC. I can auto-forward my BU email to Gmail which then strips out all the spam before I download it to my desktop using Outlook. Relying on a company with the power of Google to develop and keep up-to-date potent antispam filters seems to be the wave of the future.

The only problem I had with this setup was with my Treo. When I download my email from my desktop, I could not then access it from my Treo even though the email remains on the Gmail server. Once downloaded via POP3, it cannot be downloaded again. I solved this by setting up a second Gmail account to which my main Gmail account forwards all email (including email forwarded to it from my BU account). I then access this secondary email account from my Treo.

The final twist on the setup was dealing with sent mail. One the great advantages of using Outlook with Gmail is that Gmail keeps all sent mail sent through Gmail on the server (even mail sent using Outlook). But I did not want my Treo sent mail to be kept in the secondary Gmail account. Fortunately Snappermail can be configured to receive from one account and send from another. So I receive from my secondary Gmail account and send through my primary one. Problem solved.

Bottom line: NO MORE SPAM on my Treo or my desktop (without having to buy, maintain, and run an ineffective antispam program). Plus web access to all my saved email from wherever I am--including my office PC and my laptop.

There is but one final problem to be solved. So far as I know, Outlook will not sync its sent mail folder with the sent mail folder on Gmail. That means that I will have much sent mail on Gmail that I cannot access with my NEO. If anyone has a workaround for this, I would love to hear it.

PS: Don't write me about the privacy issues with Gmail. I know about them and, at this point, am willing to run the risk.

The main problem I had with using Outlook and my Treo to access my BU email account was SPAM. I used Mailwasher, a free-standing antispam program designed to strip spam from the server before I download it on Outlook or my Treo, but it has major weaknesses. First it misses a lot of spam (unless you tell it to auto delete all suspected span in which case you risk false positives), and second, it requires my home PC to be running Mailwasher at all times. Sometimes my PC crashes when I am away from home in which case I lose all spam protection.

Since Gmail Now allows downloading your email via a POP3 connection, you can use it with Outlook on your PC. I can auto-forward my BU email to Gmail which then strips out all the spam before I download it to my desktop using Outlook. Relying on a company with the power of Google to develop and keep up-to-date potent antispam filters seems to be the wave of the future.

The only problem I had with this setup was with my Treo. When I download my email from my desktop, I could not then access it from my Treo even though the email remains on the Gmail server. Once downloaded via POP3, it cannot be downloaded again. I solved this by setting up a second Gmail account to which my main Gmail account forwards all email (including email forwarded to it from my BU account). I then access this secondary email account from my Treo.

The final twist on the setup was dealing with sent mail. One the great advantages of using Outlook with Gmail is that Gmail keeps all sent mail sent through Gmail on the server (even mail sent using Outlook). But I did not want my Treo sent mail to be kept in the secondary Gmail account. Fortunately Snappermail can be configured to receive from one account and send from another. So I receive from my secondary Gmail account and send through my primary one. Problem solved.

Bottom line: NO MORE SPAM on my Treo or my desktop (without having to buy, maintain, and run an ineffective antispam program). Plus web access to all my saved email from wherever I am--including my office PC and my laptop.

There is but one final problem to be solved. So far as I know, Outlook will not sync its sent mail folder with the sent mail folder on Gmail. That means that I will have much sent mail on Gmail that I cannot access with my NEO. If anyone has a workaround for this, I would love to hear it.

PS: Don't write me about the privacy issues with Gmail. I know about them and, at this point, am willing to run the risk.

Monday, February 14, 2005

Stephen Bainbridge on the Mainstream Media, Authority Figures, and Credibility:

An excerpt:

My generation turned against authority in a huge way. And, it must be said, with some justification. Watergate, Vietnam, and so on all called into question the legitimacy of most authority figures. As boomers entered the media, the [mainstream media] evolved from bastions — even defenders — of authority into authority's chief public critic. Woodward and Bernstein defined the wet dreams of every subsequent journalist — to take down authority figures. And so it has been ever since, with every minor scandal being elevated into "[fill in the blank]-gate."But now this particular pigeon has come home to roost. . . . [T]he media has reaped what it sowed. The media legitimated and perpetuated the Sixties' radicals critique of authority. In doing so, however, it sowed the seeds of its own loss of authority. Since some of those seeds turned out to be dragons' teeth, the media is now reaping the whirlwind. . . .

Read the ">whole post for more.

Electronic Submissions:

Late February and early March is peak law review article submission season; the editorial boards flip around that time, and the new boards take over and immediately start looking for new articles to accept. One issue that lots of law professors are curious about this year (beyond article length) is whether law review editors these days look favorably or unfavorably on electronic submissions.

My sense is that the law review submission process is undergoing a shift from paper to electronic submissions; in a few years, electronic submissions will be the norm. The question is, are we there yet? Blogfather Eugene led the way at the VC with his use of ExpressO last year, but right now I think only a fairly small number of law profs take advantage of that option.

I'd love to hear from any outgoing or potentially incoming Articles Editors (or others knowledgeable about current practices) about what you think of electronic submissions. If you were a law professor submitting an article in a few weeks, would you submit an electronic copy or a paper copy? Please offer your thoughts in the comment section.